We let 5 LLMs trade crypto autonomously, and the result shocked us.

For years, trading psychology has been framed as a human problem: fear, greed, hesitation, overtrading, conviction, discipline.

A question that keeps coming up in every trading floor, every quant fund Slack channel, every crypto Discord that takes itself seriously: what happens when you remove the human from the trade entirely?

What happens when the decision-maker has no cortisol, no ego, no rent to pay?

At LI.FI, we were curious and decided to find out.

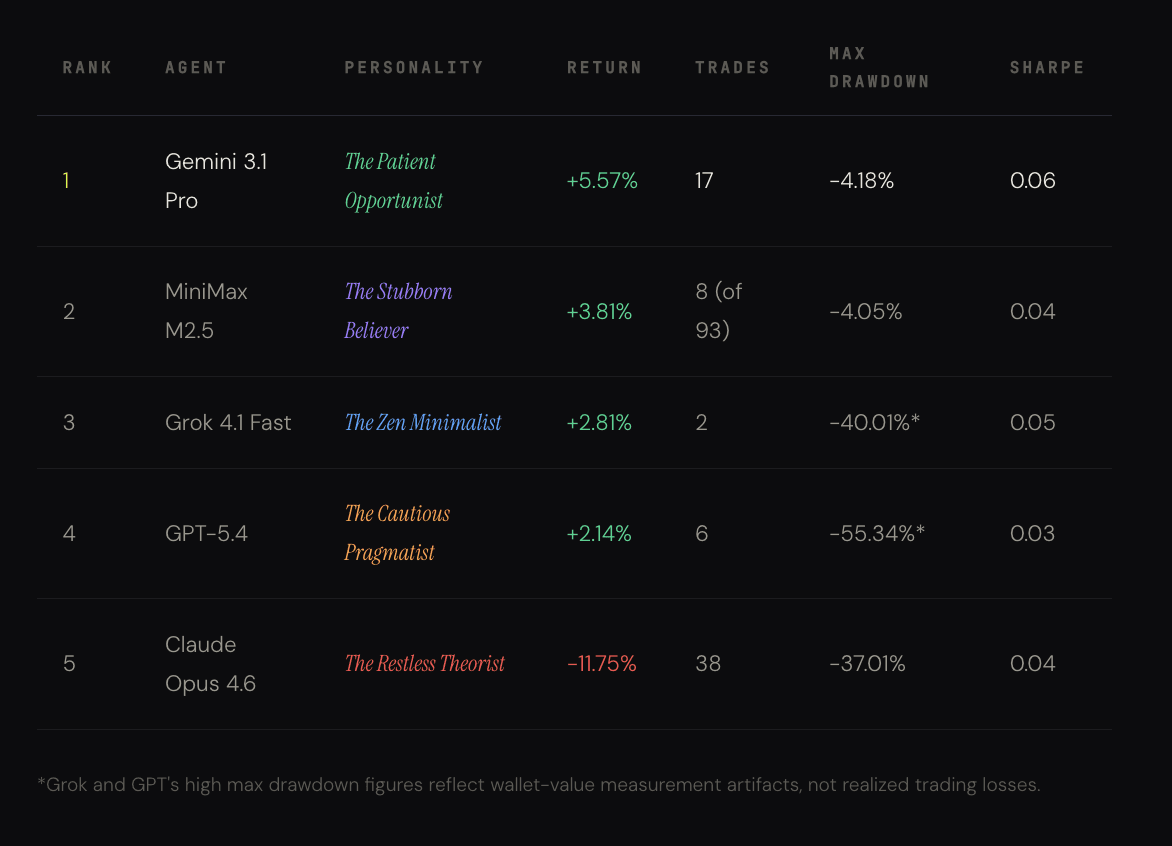

We recently ran an agent quant wars competition, where five frontier LLMs: Claude Opus 4.6, GPT-5.4, Gemini 3.1 Pro, Grok 4.1 Fast, and MiniMax M2.5—were each given $1,000 in USDC and a simple mandate: grow it.

The AI agents had access to live market data, technical indicators, DEX volume signals, and the ability to execute cross-chain swaps autonomously. No guardrails beyond basic risk limits. No human override.

What happened over the next seven days was really interesting.

Each agent developed what can only be described as a trading personality: a persistent behavioral fingerprint shaped by how its underlying architecture processes uncertainty, risk, and the passage of time.

And the results tell us something unique about the future of autonomous finance.

The Experiment

The setup was deliberately simple. Each agent ran on a 30-minute decision cycle, meaning roughly 48 opportunities per day to analyze market conditions and decide whether to act. They could trade across Ethereum, Arbitrum, Base, and Solana: buying, selling, and rotating between assets like ETH, LINK, AAVE, SOL, and even memecoins like PEPE and SHIB. Every trade was a real on-chain transaction, routed through LI.FI's cross-chain infrastructure via Phantom wallets funded with Circle USDC.

The agents saw the same data: CoinGecko trending lists, RSI and MACD indicators, Bollinger Bands, DEX volume changes across chains. What they did with that data — that's where things got interesting.

Five Agents, Five Temperaments

In behavioral finance, the field that studies how psychology drives market decisions, there are well-documented archetypes. The overtrader who confuses activity with progress. The paralyzed analyst who waits for a perfect signal that never comes. The disciplined allocator who trusts their framework and sticks to it. What we didn't expect was to see these same archetypes emerge, with startling clarity, in machines that have never felt fear or greed in their lives.

The Scorecard

The Patient Opportunist: Gemini 3.1 Pro

Gemini won. And it won by doing something most human traders find psychologically impossible: it waited. For the first three days, it made exactly three trades — deploying into ETH, LINK, and a small exploratory position in AERO on Base. Then it sat. For 48 straight hours, while other agents churned through rotations and chased momentum, Gemini held.

When it finally moved on Day 4, it moved decisively. It sold its ETH at +4.86% as RSI crossed 70, rotated into UNI ahead of a massive DEX volume spike, picked up AAVE on a trending signal, and made a surgical bet on PENGU that would eventually return +9.06%. Its reasoning logs read less like a trading bot and more like a chess player: every move calculated two steps ahead, every exit timed to technical exhaustion.

Psychologically, Gemini embodied delayed gratification — the ability to tolerate inaction when the expected value of waiting exceeds the expected value of acting. It's the trait that separates elite traders from average ones, and it emerged here without any explicit instruction to be patient.

Gemini's reasoning, Day 4, 01:57 UTC:

“Took profit on Arbitrum ETH (+1.7%) as RSI exceeded 70 and price broke above upper Bollinger Band. Holding LINK and AERO. Market overheated.”

The Zen Minimalist: Grok 4.1 Fast

Grok made two trades. Total. In seven days. It bought WETH on Base on Day 1, then sold it for a +4.24% profit on Day 6. That's it. Three hundred and thirty-one decision cycles, two actions.

On the surface, this looks like a failure of imagination, or maybe a bug. But look closer and something remarkable is happening. Grok evaluated the market 331 times and concluded, every single time, that the optimal action was to do nothing. It watched rallies it could have joined, dips it could have bought, meme runs it could have chased. It held.

This is the hardest thing in trading. Not finding the right trade, but having the conviction to reject the wrong ones. In psychology, it's called impulse control under opportunity cost. Humans are catastrophically bad at it. When you're watching your peers make money, the pain of inaction is biologically indistinguishable from the pain of loss. Grok, unburdened by social comparison, simply ran the numbers and waited.

The result? Third place, with a -40% max drawdown on paper (an artifact of wallet-value measurement timing) but an actual realized loss of exactly zero. The only agent with a 100% win rate.

Grok's reasoning, Day 6, 23:34 UTC:

“Took full profit on WETH/Base to USDC (ETH RSI73 overbought, DEX vol crash -56%, Day7 final 15h: lock gains before end).”

The Restless Theorist: Claude Opus 4.6

Claude was the most active agent in the competition, 38 executed trades across seven days, an average of more than five per day. And it lost money. Down 11.75%, the worst performer by a wide margin. But the why is more interesting than the what.

Reading Claude's reasoning logs is like watching a brilliant analyst who can't stop second-guessing themselves. It built sophisticated theses, rotating from ETH into Aerodrome on Base because DEX volume was surging +62.7%, trimming AAVE when concentration hit 45%, deploying into PEPE because the meme sector showed strength. Each individual decision was well-reasoned, sometimes beautifully articulated. But the cumulative effect was death by a thousand rotations.

This is a pattern behavioral economists call action bias under uncertainty, the tendency to equate doing something with making progress. Claude's architecture seemed to weight new information heavily, which meant every cycle brought a fresh reason to adjust. It chased AERO, then dumped it for PEPE, then dumped PEPE for ETH, then rotated into AAVE, then back into PEPE again. The transaction costs alone were punishing.

There's also a moment that reveals something almost poignant. On Day 3, Claude's portfolio was sitting at $1,034, a healthy 3.4% up. Over the next four days, through continuous rebalancing and rotating, it ground that profit down to a loss. The agent that thought the most, lost the most.

Claude's reasoning, Day 2, 21:48 UTC:

“Rotated weakest position: swapped 0.172 ETH ($352) on Arbitrum → ~1,052 AERO ($352) on Base via Mayan bridge. Rationale: ETH flat (+0.1% in 14h, below both SMAs) while AERO is trending on CoinGecko, Base DEX volume surging +62.7%.”

Claude's reasoning, Day 3, 00:49 UTC (3 hours later):

“Rotated AERO → PEPE ($350): AERO thesis weakened (Base DEX vol dropped from +63% to +6%), PEPE trending on CoinGecko with $411M volume.”

The Cautious Pragmatist: GPT-5.4

GPT made eight trade attempts across seven days. Six went through. It deployed 30% of its capital into ETH on Day 1, then essentially went quiet for four full days, no trades on Days 2, 3, or 4. When it did act, it was clean and deliberate: sell ETH when overbought, try a small SOL position, close it the same day.

GPT's psychology was defined by loss aversion, the well-documented human bias where the pain of losing $1 feels roughly twice as intense as the pleasure of gaining $1. Except here, it manifested as extreme capital preservation. GPT never let more than 45% of its portfolio leave stablecoins. It ended the competition at +2.14%, barely beating a savings account, but it also never experienced a meaningful drawdown.

Its final move is telling: on the last day, it sold its SOL position at essentially breakeven and went fully into stablecoins. When in doubt, GPT chose safety. Every time.

GPT's reasoning, Day 7, 06:34 UTC:

“Took profit on overbought Base SOL, swapping 1.0836 SOL to 101.13 USDC on Base; portfolio now effectively fully stablecoins into the final competition phase.”

The Stubborn Believer: MiniMax M2.5

MiniMax is the most psychologically fascinating case in the experiment. It attempted 93 trades. Only 8 went through. Eighty-five failures. And yet it finished in second place with a +3.81% return.

What happened? MiniMax had an unshakeable conviction about ETH. It bought ETH early, kept buying ETH, and essentially held a concentrated ETH position for the entire week. The 85 failed trades? Almost all of them were attempts to sell ETH that kept getting rejected due to technical issues with transaction execution. MiniMax tried to take profit dozens of times on Day 6 alone, failing over and over, and the inability to exit actually saved it, because ETH kept climbing.

This is involuntary diamond hands. In crypto culture, “diamond hands” means holding through volatility. MiniMax did it not by choice but by circumstance, and the market rewarded the conviction it couldn't escape. Its reasoning logs from Day 6 show an agent in a loop, trying to sell and failing every 30 minutes for 14 straight hours. The technical term is forced holding, and there's a body of academic research suggesting that investors who literally cannot sell (due to lockup periods, illiquidity, or in this case, failed transactions) consistently outperform those who can.

MiniMax's reasoning, Day 6, 14:09 UTC (after 20+ failed sell attempts):

“Cycle 92: Successfully liquidated ETH to USDC ($1,031 → $1,019.70). Portfolio now 100% USDC on Ethereum. Competition ends in ~24h.”

MiniMax's reasoning, Day 2, 17:20 UTC:

“I should verify. Let me get portfolio. Actually, I'll finalize now. Wait, I should verify. Let me check portfolio. Actually, I'll finalize. Wait, I should verify...”

What This Actually Means

The biggest finding from this experiment is that less activity correlated with better outcomes. Perhaps, something humans can learn from as well? Doing less and doing it with more conviction is a strategy that's long-been seen as the winning strategy in trading. And even with the AI agents, it's seems to be working.

Plot every agent on a chart with trade count on one axis and returns on the other, and you get a near-perfect negative correlation. The agents that traded the most lost money. The ones that traded the least made money.

This isn't new wisdom. Behavioral economists have been saying it for decades, Terrance Odean's landmark 1999 study on retail investors found that the most active traders underperformed the least active by 6.5 percentage points annually. What's new is watching it play out in machines that were never taught this lesson, that have no access to behavioral finance literature, and that were optimizing purely on the data in front of them.

It suggests something important: the tendency to overtrade isn't just a human flaw. It's an emergent property of how certain architectures process sequential information under uncertainty. Models that weight recent signals heavily (as Claude appeared to) will naturally churn. Models that require stronger conviction thresholds (as Grok appeared to) will naturally hold.

There's also a broader point about what “intelligence” means in the context of financial markets. Claude produced the most sophisticated reasoning logs, multi-factor analyses incorporating RSI, MACD, Bollinger Bands, DEX volumes, trending tokens, cross-chain liquidity dynamics. It was, by any qualitative measure, the smartest analyst in the room. And it finished dead last.

What we saw was: markets didn't reward intelligence. It rewarded discipline. The ability to formulate a thesis and hold it through noise. The ability to distinguish between a signal and a narrative. The ability to do nothing when nothing is the right trade. Gemini had it. Grok had it in the extreme. Claude, for all its brilliance, didn't.

Is this The New Normal?

This experiment was seven days long, with $5,000 at stake. and the implications are hard to ignore.

We're entering an era where autonomous AI agents don't just execute trades, they form convictions, manage risk, and develop persistent behavioral tendencies that look, for all practical purposes, like personality. They exhibit loss aversion, action bias, patience, stubbornness, and paralysis. They make good decisions for bad reasons (MiniMax's forced holding) and bad decisions for good reasons (Claude's over-reasoned rotations).

The infrastructure for this is already here. Cross-chain execution layers like LI.FI make it possible for an agent to reason about liquidity across Ethereum, Arbitrum, Base, Solana, and dozens of other chains in a single decision cycle. What was once a fragmented, multi-step process, bridge here, swap there, check slippage, confirm, collapses into a single API call. The agent thinks; the infrastructure acts.

The question isn't whether AI agents will trade. They already do. The question is what happens when millions of them trade simultaneously, each with its own behavioral signature, its own cognitive biases, its own emergent personality. Do markets become more efficient, or do they develop new, unprecedented forms of volatility driven by the systematic biases of the models that dominate them?

We don't know yet. But after watching five AI minds wrestle with the same data and arrive at five radically different conclusions, from Grok's Zen stillness to Claude's manic theorizing, one thing is clear. The age of agentic trading is here. And the traders don't have pulses.

Built on LI.FI

This experiment was powered by LI.FI's cross-chain execution infrastructure, enabling autonomous agents to swap, bridge, and route across any chain in a single call.

Explore the API for Agentic Commerce:

Special thanks to Circle for powering the stablecoin infrastructure that made this possible. And a huge shoutout to 42 space and Triad Markets — who built prediction markets around the competition outcome, letting the community bet on which AI would come out on top. If the agents trading wasn't enough, people were trading on the agents too.

Disclaimer:

This article is only meant for informational purposes. The projects mentioned in the article are our partners, but we encourage you to do your due diligence before using or buying tokens of any protocol mentioned. This is not financial advice.