Tokenized Stocks Supercycle

Introduction

It’s 2050. All stocks are tokens. It is laughable that stocks were not tokens before. You, reader, are early, because you’ve been purchasing stocks in the years before tokenization, which feel like the years before the internet.

The future of finance is changing quickly because the way we coordinate as humans is changing. We live during a time that feels like the future, embedded with LLMs and WIFI and screens. Crypto continues to be a massive part of this shift towards faster coordination, focusing on value.

The tokenziation of stocks is the next paradigm shift that blockchain technology will change the world through. This essay is a primer on that.

Stablecoins Walked so Tokenized Stocks Could Fly – And the World Will Never Be The Same

Tokenized stocks are the perfect amalgamation of legacy, fintech, and crypto rails, embedding the assets of capitalism with the freedom of anarchy to ensure that the most in demand items can trade 24/7/365 globally while bypassing the friction of unstandardized timezones, regulations, and file formats.

In the grand scheme of crypto adoption transforming how value is represented in the world through tokenizing everything, tokenized stocks are the obvious successor for mass adoption to stablecoins, aka dollars as tokenized dollars (or digital dollars). It is a natural progression that feels unnatural now, in the moment of invention, but stablecoins followed the recreation of commodities as digitally native entities (bitcoin and eth) as well as wrapped commodities like tokenized gold -- stocks are the obvious next man up. The pitch is that stocks and ETFs are some of the most demanded financial assets in the world, and blockchain rails can make them more accessible, more composable, and eventually more useful inside the internet financial system.

If you had asked someone in 2020 about stock tokenization and who would win, the answer might have been Coinbase or FTX. In 2026, our predictions fall far short of our wildest dreams -- because the players looking to win the tokenization of everything are now fighting an arduous battle of voting rights, transfer agent hopping, settlement windows, and regulatory arbitration are not just limited to the crypto natives that are so used to pushing the boundary of what can be and what is legal. No, the players in the tokenized stock battle are big, the final bosses of finance, starting with Robinhood and NYSE and NASDAQ and ICE Markets and the DTCC, along with the crypto natives orgs that have a head start like Ondo, xStocks, Backpack, and those somewhere in between like Binance and Coinbase.

This article is about tokenized stocks, why we should be excited about them, and who the big players are that we need to be paying attention to.

Before we talk about tokenized stocks, it’s worth taking a step back and asking – what is a stock?

What is a Stock?

Stocks and stock markets emerged to coordinate a coincidence of wants in the universe: businesses needed a way to raise capital for their expenses and expansion, and the public needed a way to gain exposure to the growth of these businesses.

This led to the formation of the concept of stocks, which would allow businesses to raise capital by turning ownership in them into tradable, units of liquidity - called stocks.

The earliest example of stocks being used to fulfil this coincidence of wants is the Dutch East India Company, who back in 1602, which raised capital by issuing stocks that could be bought by the citizens of Dutch Republic. These stocks could then be traded in secondary markets, one of which eventually became the Amsterdam Stock Exchange. Almost two centuries later, in 1792, the Buttonwood Agreement laid the foundation for what became the New York Stock Exchange - where different market participants could trade stocks of all US-based companies under set rules and regulations.

So the simplest definition of a stock is that stocks represent exposure to the upside/downside of the business. In legal terms, this exposure came to be termed as 'ownership' in the company, which, in the regulated traditional financial markets, also gives stock holders (or shareholders) certain rights such as voting or a right to participate in corporate actions, such as getting a share of profits of the company in the form of dividends.

From a technology standpoint, stocks are still relatively new. They are less than 500 years old, and the penetration of stocks into the hands of the average person is even smaller. In the great U.S. stock market crash of 1929, fewer than 2.5% of Americans owned stock directly. Today, that number is much higher: stock ownership is closer to 62% in the U.S. - largely because of retail friendly fintech products and brokerage platforms, which have made buying stocks easier and more accessible for the average person. But that number is still so low!

Tokenized stocks are the next step in that long distribution curve - and expand the total addressable market of stocks from domestic markets to a global one, changing the entire landscape forever.

We should not think about tokenized stocks as just putting the same asset on blockchains. Instead, we should think about tokenized stocks as the technological innovation that changes how the average person gains exposure to businesses globally.

What are Tokenized Stocks?

At the simplest level, in their current form, tokenized stocks are blockchain-native assets that track the value of publicly traded equities or ETFs.

The exact legal structure and token format differs by issuer. Some are tracker certificates, some are derivatives, some are issued through special purpose vehicles (SPVs), and some may evolve toward more direct ownership models over time. But the general idea is the same for all of them: a user holds a stock that exists as a token on a blockchain that gives them economic exposure to an underlying stock or ETF.

This token, therefore, is compatible with legacy systems through the issuer, the blockchain through the token format, and, if compatible with an interoperable token standard, all blockchains through a token extension format like Omnichain Fungible Token Standard (OFT) or Cross-Chain Token Standard (CCT) that enables assets to be issued, moved, and held across every type of blockchain.

As I said earlier, this is a beautiful amalgamation of legacy, fintech, and crypto rails. However, in the bull case for tokenized stocks, there will come a day when tokenized stocks are the native version of the equity itself. In that world, the tokenized stock is not tracking a stock listed on a traditional stock exchange. It lives natively onchain and represents the equity itself.

The best versions of the tokenized stocks generally have three core properties:

1. 1:1 collateralized exposure to stocks

Tokenized stocks are 1:1 collateralized, meaning an equal amount of stock supply that is tokenized on blockchains is kept in the traditional finance system off-chain in custody accounts of brokerage firms. This is done in order to offer guarantees to the investors that the tokenized stock they’re buying is backed by the real deal, held in custody off-chain.

In the early days of crypto, tokenized stocks gave economic exposure with no further shareholder rights to the investors. Today, 1:1 parity is industry standard and more rights are being baked in by the day. As complexity of issuers continues to increase, this should become the norm. For instance, in most issuer models today, in the case of corporate actions such as dividend distributions, stock splits, and other special events, adjustment mechanisms exist to reflect those changes for token holders and preserve parity with the underlying asset.

2. Blockchain-native, and hence internet-native, accessible 24/7

One of the main features of tokenizing stocks is unlocking global access for these assets. Traditional equity markets are still fragmented by geography, brokerage relationships, settlement systems, market hours, and local regulations. For many global users, buying U.S. equities is difficult, expensive, or simply unavailable through local financial infrastructure. Putting stocks onchain changes the distribution model of stocks. Tokenizing a stock makes the asset globally available, instantly, they go from being limited to domestic markets to globally accessible stocks instantly. A tokenized stock can be held in a wallet, transferred between venues, routed through onchain liquidity, and surfaced inside apps that already serve crypto users.

For instance, with the SpaceX IPO and the launch of tokenized SPCX across blockchains, it was the first time I, being an Indian national, could legitimately see how I can get exposure to the asset so easily on blockchains. I don’t have to go through all the hoops in the traditional financial system that I would otherwise have to, and which would eventually lead to me not taking the opportunity because of all the friction in between. That is the unlock: anybody, anywhere, with just an internet connection can gain exposure to stocks that are issued in a totally different jurisdiction.

That does not mean every tokenized stock is permissionless or available to everyone. In practice, many products still have restrictions, onboarding requirements, and jurisdictional limitations. But the distribution model is still fundamentally different from traditional brokerage. Instead of every user needing a brokerage relationship, every wallet, exchange, fintech app, and DeFi interface can become a potential access point.

3. Composability across the DeFi ecosystem - using stocks as money, collateral, and for payments

Potentially the biggest unlock of tokenizing stocks is the DeFi primitives and markets that can be built with these assets across blockchains.

Effectively, tokenizing a stock makes it money, which means that it can now be used and re-used across different financial markets and even as a medium of exchange of value, in the form of money. Tokenized stocks allows stocks to be used as collateral, paired in liquidity pools, integrated into structured products or included in automated strategies or even used for payments. This is where tokenized equities stop being a brokerage wrapper and start becoming net new financial primitives that can only exist on blockchain rails and within the DeFi ecosystem.

However, today most tokenized stocks are still very early and are in fact wrappers of stocks in the traditional markets. This is not meant as a dig. Getting to this stage means overcoming a lot of traditional market friction points and solves the cold-start problem of tokenized assets. But it is also fair to say that the main benefit of early-stage tokenized stocks is access and trading on blockchains. It is when they get integrated across DeFi, they will truly realise the benefits of being tokenized assets as it will open up new financial models and revenue streams for the asset issuers. The more these tokenized stocks get integrated into DeFi products, the more liquidity they attract, and the more useful they become. The more useful they become, the more DeFi integrations they attract. The more integrations they attract, the more distribution they get. That is the flywheel long term of tokenized stocks.

Why Tokenized Stocks Could Be the Next Big RWA Category

Tokenized stocks have been around for a few years, but there’s a reason why everyone is excited about their long-term future. It’s because, now, it’s actually different, different in terms of regulations.

The same way stablecoins were shadowed by regulatory uncertainty for years, regulatory uncertainty loomed large over tokenized stocks, and the real-world assets category more broadly. What does the legal structure look like? What are the token holder rights? How do we ensure investor protection? All of these, and more, were open-ended questions that are only now getting some clarity.

That cloud of regulatory uncertainty is slowly fading away with tokenized stocks. And we’re seeing companies move at unprecedented speeds. From the crypto natives like Ondo, xStocks, and Backpack, to centralized exchanges like Coinbase and Binance, to the heavyweights of the financial world with DTCC, ICE, and Robinhood, we’re seeing tremendous activity across the spectrum.

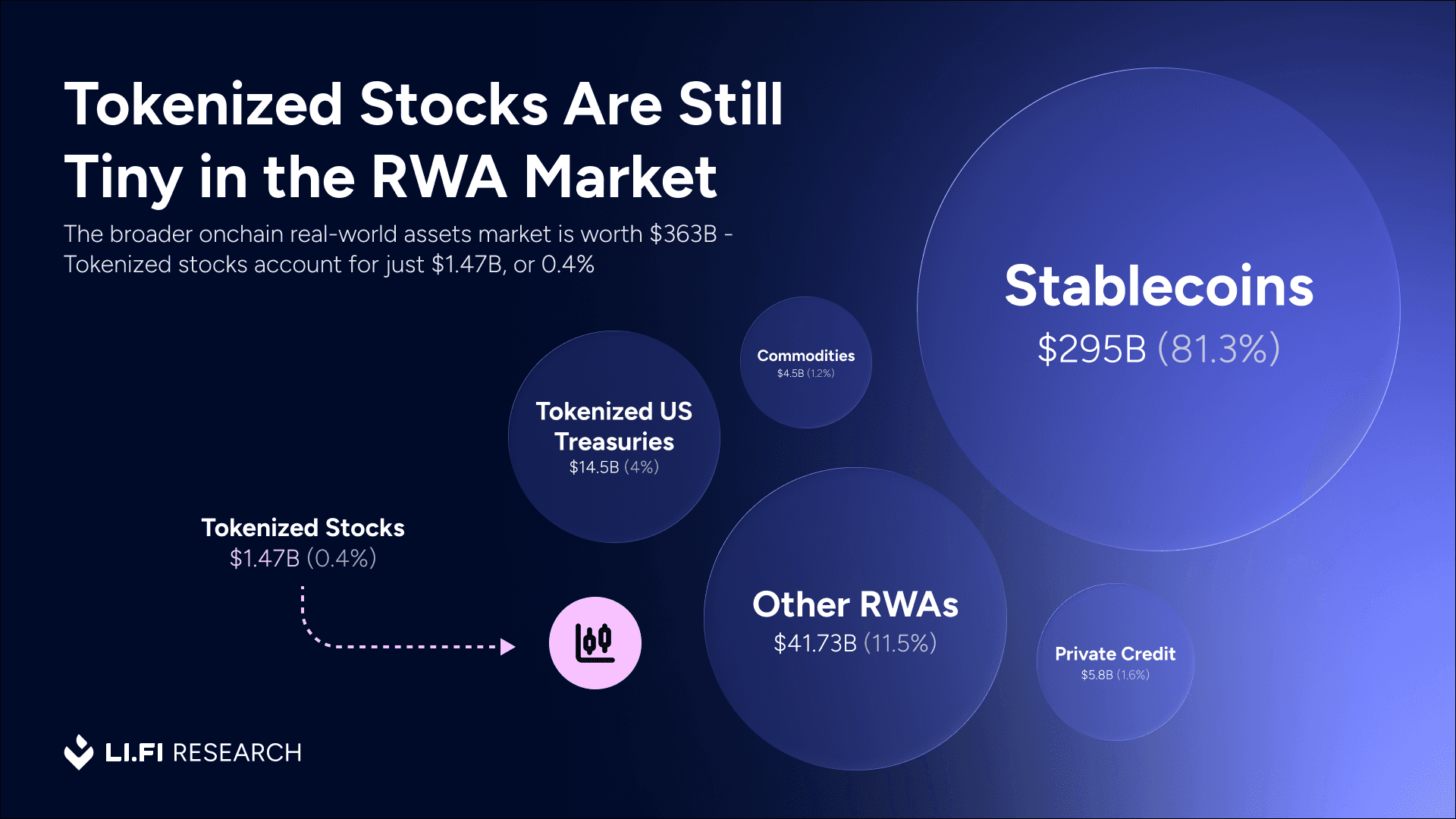

However, it must be noted that despite all the excitement, tokenized stocks are still tiny relative to the broader real world assets market which is around $363B in asset value.

Stablecoins remain the dominant real-world asset onchain with $295B in tokenized value commanding over 81.3% of the real world assets value onchain, but even among the other categories, there are real-world asset categories like tokenized US Treasuries ($14.5B, 4%), Commodities ($4.5B, 1.2%), and Private Credit ($5.8B, 1.6%) that have seen more development in comparison - Tokenized stocks are still early at 1.47B and 0.4% represents only a small fraction of the overall RWA market. That is exactly why the category is interesting.

Note: as per data recorded in early July 2026, source: RWA.xyz

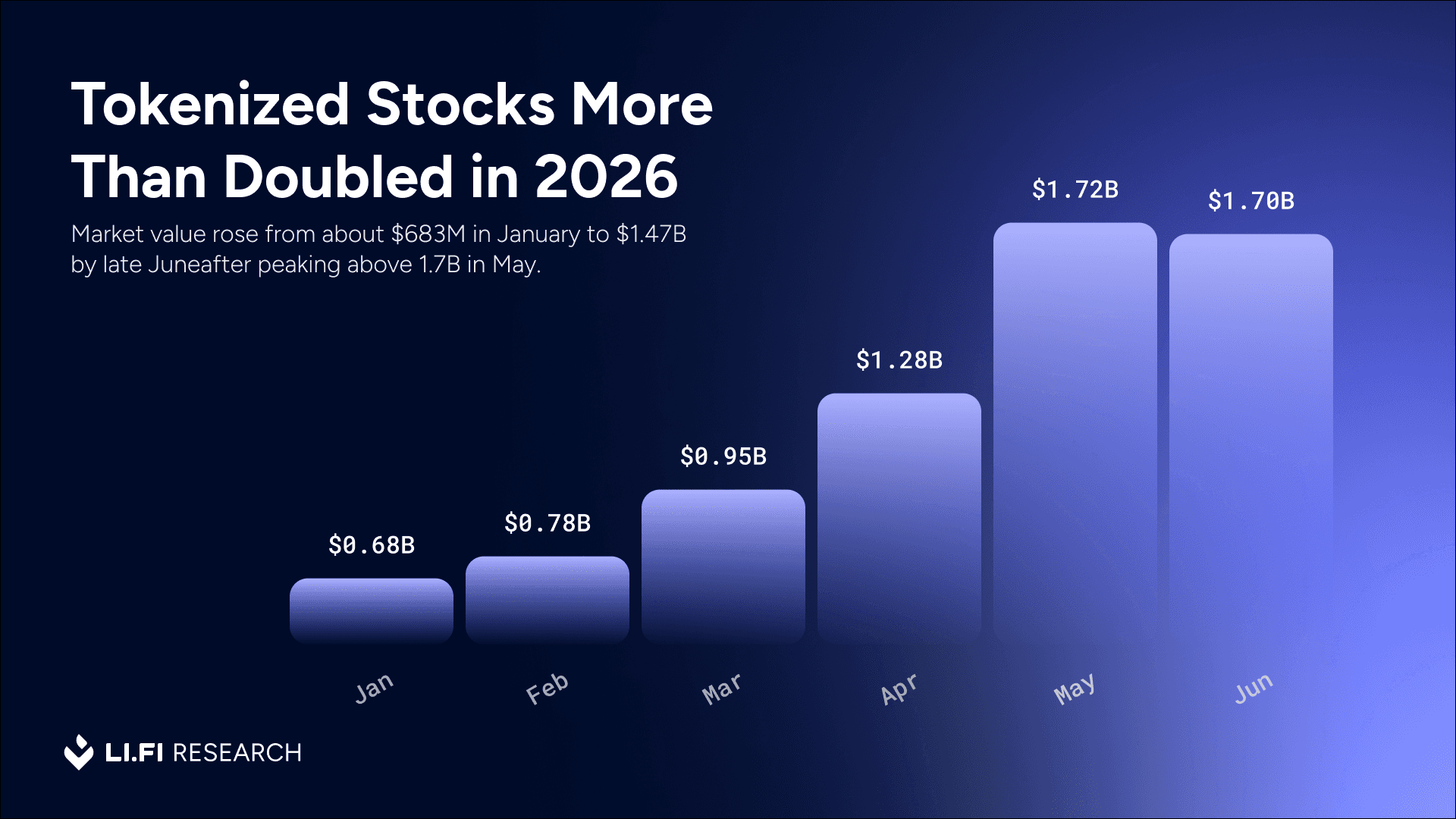

That is exactly why the category is interesting. Tokenized stocks are still small enough to have enormous upside, but they are now large enough to show that there is real demand.

The adoption of tokenized stocks accelerated in 2026. The category more than doubled from ~$683M at the start of the year to ~$1.47B by late June, briefly peaking above ~$1.7B in May. In less than six months, tokenized stocks added almost twice as much value as they did during all of 2025.

This is partly because of how global markets have shaped up this year. Everything other than commodities and U.S. stocks has been largely deprived of liquidity and attention. Crypto markets themselves have seen liquidity move out of the ecosystem, and other than the interest around Zcash and Hyperliquid, not much has tickled the fancy of crypto investors.

When you look at this market structure, it’s clear that the attention of the world has shifted toward the U.S. stock market. And now is also the time when some of the most hyped names, or tickers with retail attraction, are going for IPO. SpaceX is one recent example. So naturally, there’s demand for these assets from crypto and non-crypto investors alike. Putting them onchain has opened up a potential new market, and perhaps given us a glimpse of what NASDAQ onchain could really look like.

While tokenized stocks are inevitable, 2026 brought the clearest signal that this category has real potential and made the promise obvious to the broader ecosystem. 2026 is the year that will be remembered as the year everyone saw what the future could look like with tokenized stocks.

Note: as per data recorded in early July 2026, source: RWA.xyz

Tokenized Stocks Winners and Losers Will Genuinely Affect The Future of Finance

Global equities is a $150 trillion market, and tokenized stocks are barely at $1.5 billion. So when we say we’re early, we’re really freaking early in the tokenized stocks era. The access and capital efficiency benefits of tokenized stocks are undeniable, nobody ever really doubted that, but it’s good to finally have proven demand to really get the ball rolling.

In terms of issuers of tokenized stocks, there’s a wide spectrum of players, from crypto natives to incumbents, all trying to make a place for themselves in the issuance game. Depending on which side of the spectrum you’re looking at, they are either trying to set a new world order of finance or preserve the existing one.

Crypto Native Issuers

On one end of the spectrum, we have crypto-native companies like Ondo, xStocks, and Backpack.

Currently, the crypto-native issuers are joint to the hip with the incumbents connected through brokerage firms (like Alpaca) as the stocks natively live in traditional financial markets, and the crypto-native issuers offer a 1:1 representation of the stocks onchain.

The models and guarantees each team has adopted are also different, and each has its own pros and cons. But they are all tokenizing assets in a way where they issue “wrapper” tokens of traditional stocks. This basically means that the native asset, which is the traditional stock, still lives offchain in traditional markets and in the custody accounts of traditional brokerage firms. What they issue onchain is a token that offers exposure to the stock and guarantees in the form of 1:1 backing.

Depending on the issuer in question, there are also guarantees that allow you to either sell the onchain tokens into stablecoins or cash, or the underlying stock itself with brokerage firms.

Exchanges & Fintechs

In the middle of the spectrum, we find crypto exchanges like Coinbase and Binance, and fintech giants like Robinhood. These players sit at the intersection of distribution for investment capital.

The centralized exchanges sit between crypto-native users and the average stock investor who is crypto-curious. The Robinhoods of this world have found a place for themselves by catering to a new generation of investors, while also actively expanding their product suite to capture market share and users on both ends of the investment spectrum. They want the conventional retail investors in the traditional finance world, but they’re also dipping their toes into the user base of centralized exchanges by expanding their crypto offering. And not just that, they’ve also launched their own chain and tokenized stocks offering that settles on it, going after crypto-native users directly.

These players have already made their mark in the global world order of finance, and it makes total sense that they would all want to own a chunk of the tokenized stock market as well. They have the distribution, they sit at the intersection, and they may in fact turn out to be the perfect platforms for the right target user who, at the end of the day, ends up buying tokenized stocks.

Legacy Market Infrastructure

Then there are the incumbents like Intercontinental Exchange, or ICE, which owns NYSE, and Depository Trust & Clearing Corporation, or DTCC. These are some of the biggest players in the current market structure of equities in the U.S., and they have already publicly announced their plans to build tokenization platforms, with the likes of DTCC launching their Tokenization Service later this year.

These companies hold a lot of the power in determining the fate of tokenized stocks, and tokenized real world assets more broadly, because these are the companies that hold the assets in traditional markets - and thus hold a lot of leverage in deciding how and when these assets will be tokenized onchain.

Every firm will have their own approach, but current signs suggest that incumbent players will be adopting a mix of tokenizing stocks on their own blockchain and a handful of others that operate within the perview of regulations (like Canton), while the broader mutli-chain ecosystem expansion of tokenized stocks will be done via crypto-native issuers. This way, the incumbent tick many of their boxes. They meet the regulatory requirements that already exist today, they keep control of the issuance layer and maintain the current status quo that favors their position, and they benefit from the capital efficiency and new investors that tokenizing stocks on blockchains unlocks.

Everyone is sprinting to tokenize everything. There will be winners and losers, but mostly, there will be tokenized stocks. That much feels certain.

Conclusion

In conclusion, the tokenized stocks market is still very early, but now we have seen enough adoption to prove that demand exists. It is one of the most exciting and fastest-growing RWA categories because it has three major advantages:

It is the product that’s the easiest to understand for everyone. Everyone knows what stocks are. A tokenized Nvidia or Tesla product is much easier to explain than tokenized private credit, tokenized receivables, or tokenized real estate debt.

They are naturally liquid assets. The underlying stocks already trade in deep global markets. That gives tokenized stocks a better starting point than many RWAs, where the underlying asset itself is illiquid or difficult to price.

They are culturally relevant, retail-friendly assets. Crypto is a market driven by attention, and equities have attention. AI stocks, IPOs, megacap tech, meme stocks, and private-market access all create demand that can spill into tokenized versions of those assets.

The SpaceX IPO showed how quickly tokenized equities can capture attention. SpaceX-related tokenized stock products drove meaningful onchain activity across multiple issuers and venues:

SPCXon surpassed tens of thousands of trades on Ondo Global Markets, crossing $1M in volume in an hour.

Solana spot markets reportedly did $37M in day-one volume.

Backpack’s SPCX crossed 10,000 holders on Solana and $350M in cumulative onchain volume.

xStocks’ SPCXx reaching more than $200M in monthly transfer volume.

More broadly, SpaceX helped push onchain tokenized-stock trading volume to a record $4.3B over a 30-day period.

This is why tokenized stocks act as the wedge to get broader interest into the category and get real world assets more widely available across all the trading avenues on blockchains.

Stablecoins in many ways have written the playbook, and there’s a world where tokenized stocks can follow the same path towards mainstream acceptance and adoption. There is a world where traditional finance brokerage firms just list tokenized stocks because the margins are better. Now it will take years if not a decade or more for this to play out, but hey at least there’s hope and sometimes that’s all we need to bring some attention back to the crypto ecosystem, which currently is crying out for attention and liquidity as we find ourselves in the depths of this never ending bear market. Perhaps this is what early product-market fit looks like for tokenized stocks.

However, as tokenized stocks gain early traction, the market is also starting to show the problems typical of any early-stage financial market structure: fragmentation.

For tokenized stocks, that fragmentation exists primarily across asset issuers, blockchains, liquidity venues, and distribution channels. This can quickly become complicated for consumer crypto applications, which may not want to integrate with every issuer, venue, or blockchain individually just to offer users access to tokenized equities. As a result, fragmentation can become a bottleneck for distribution.

This is where LI.FI comes in. LI.FI is the distribution layer for tokenized stocks.

At LI.FI, we provide the rails for trading all assets and currently support hundreds of tokenized stocks across multiple issuers like xStocks, Ondo, Backpack, Robinhood, Coinbase, Binance, and others.

We expect this number of tokenized stocks and issuers to explode and are building infrastructure to support this, but that is not the point of this essay, so we will leave it at that.

…

Disclaimer:

This article is only meant for informational purposes. The projects mentioned in the article are our partners, but we encourage you to do your due diligence before using or buying tokens of any protocol mentioned. This is not financial advice.